The Dizzying Rise of Cloud Lending Platforms in India - A Technologist’s Perspective

Bank CEOs now 'think themselves as running technology companies, as much as they do about running financial companies'

India is going through a Fintech revolution. With the world’s highest adoption rate of 87% [2] and the Government’s support through programs like UPI, India Stack and Jan Dhan Yojana - India is at the start of a Tech-driven Financial services boom.

Up until recently, Banks and NBFCs used proprietary legacy software to process lending applications. Today, with the near-ubiquity of Cloud service offerings, Cloud lending is becoming a desirable proposition.

In this blog, I wish to talk about why cloud lending is a better proposition when compared to legacy on-premise lending systems. We’ll cover just four main aspects today. Let’s dive in.

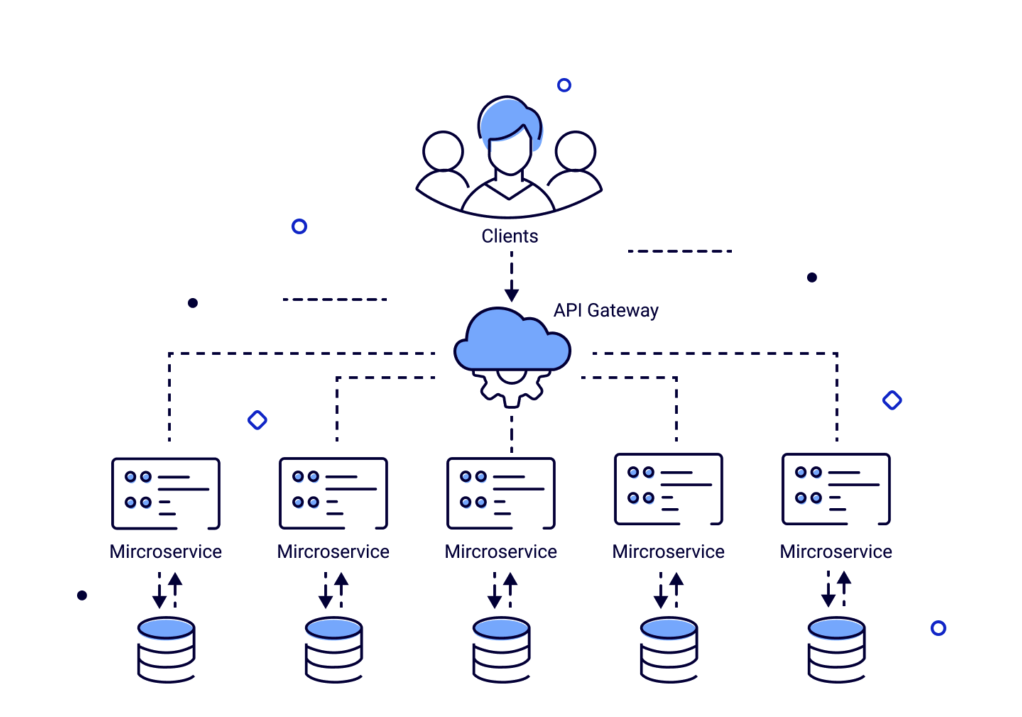

Microservices Based Architecture

Most legacy banking applications are monolithic systems with tight coupling between modules. This made sense when all the data to be processed was within the bank systems. With the advent of Open APIs in India’s financial sector (especially India Stack), banks have access to much more information to process loans.

Old monolithic systems are limited in their functionality to make most of these Open APIs. What is needed is a Microservices-based architecture where each module is loosely coupled with other sub-systems.

Cloud-native applications are generally designed on microservices architecture, making them highly configurable. This gives Cloud lending platforms an extra edge as they can quickly adapt to newer changes in the OpenAPI ecosystem.

Since each microservice is independently scalable, it becomes easier for banks to scale individual modules to access newer markets and data without affecting the rest of the system.

This capability to scale allows the Cloud lending platforms to create High Availability systems that respond to requests within milliseconds irrespective of traffic volume. High Availability capability is further boosted with features like Availability Zones.

Availability Zones form logical zones across multiple data centres in multiple geographies. These logical demarcations are defined within the laws and regulations of the respective countries/regions.

These Availability Zones help us in designing reliable and resilient applications that automatically transition between physical zones without any interruptions. Such availability zones are more scalable and fault-tolerant than traditional single data centre setups.

One of the most popular use cases of Cloud lending services is the Cloud-native Loan Origination System (LOS) platform, which helps take lending decisions in seconds. The platform allows lending institutions to go completely paperless and make loan processing a breeze.

Efficient processing is achieved by using Advanced Load Balancing techniques like Circuit Breaking and Backpressure Request Handling. Even during downtime scenarios, a microservices architecture is highly resilient. It is pretty easy to spin up a new replica without affecting other microservices as much.

In the competitive FinTech world where time is of the essence, on-premise legacy systems have scalability limitations, making the customer switch to competitor offerings.

There are other benefits as well of a microservices architecture. Since applications are split into smaller parts, they are easier to build, optimise and maintain. Each microservice has its own software ecosystem. This means they can be coded in the programming language that is best suited for its functionality.

Containerisation Benefits

Containers are ubiquitous in Cloud-native applications. Micro-services architecture goes hand-in-hand with containerised setups. On-premise legacy applications often do not fully exploit the containerisation benefits, even when they use it.

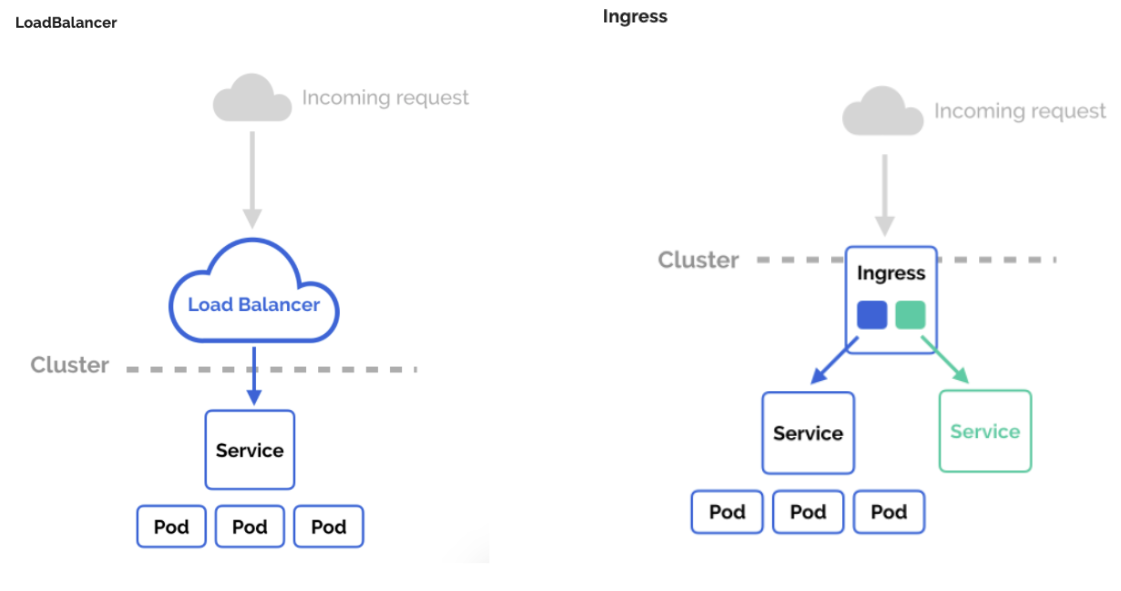

A case in point is Container Ingress.

Every lending application requires a set of services from its infrastructure, for example, decision-making system, traffic management, data processing, health monitoring, security compliance, user authentication etc. These services are often implemented as discrete applications.

An optimised service infrastructure requires traffic management not only east-west in the data centre but also north-south within each discreet application. Traditionally, this happens with a mix of Load balancers and queuing systems within the applications.

To expose any service, one has to create a new LoadBalancer and get an IP address. But this leaves many points of failure in the system.

By contrast, in a Cloud-native lending platform, a lot of traffic management between services is taken care of by Ingress systems like Kubernetes Ingress.

Kubernetes Ingress is an entirely independent resource that allows access to services from outside the cluster. One can configure access to define which inbound connections reach which services. This makes it isolated from the services being exposed.

Container Ingress also helps in consolidating all routing rules into one place.

Cloud lending platforms take benefit of this feature inherently due to the use of microservices-based architecture. This over a long period means more optimised use of computing resources and fewer chances of failure.

Better Deployment Strategies

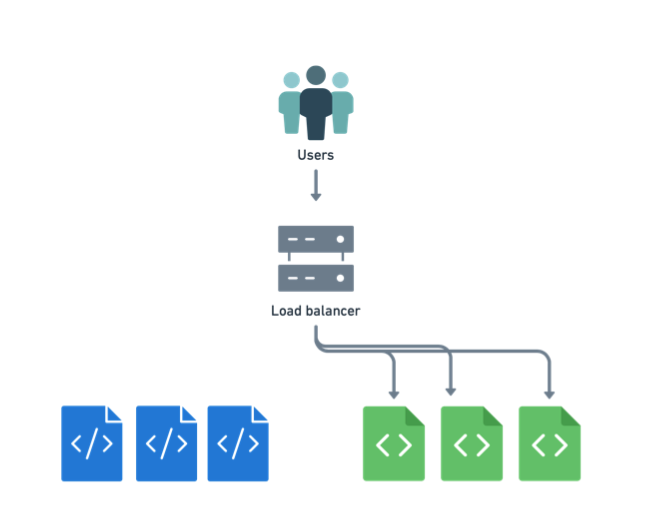

Blue-Green deployment is a popular release management strategy. It uses two production environments in parallel. Since there are two versions live at a time, it provides an opportunity for reliable testing, no-outage upgrades and instant rollbacks.

However, performing a Blue-Green deployment in an on-premise setup can be very expensive. We have two parallel production environments and thus use double the required capacity for a blue-green release cycle. It can increase CapEx significantly.

Cloud lending platforms can provide the same functionality for a fraction of the cost. Cloud resources are theoretically limitless. This means that a Blue-Green deployment is easily possible in a Cloud setup by expanding capacity only for the period of the release cycle.

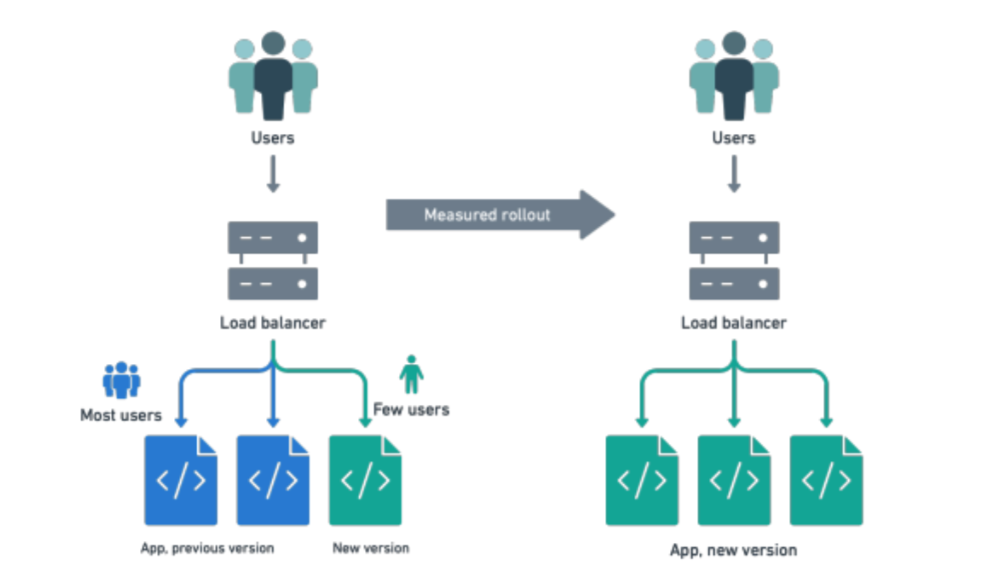

Taking it a step further is the Canary deployment technique. In this, only a part of the traffic is diverted to the newer version. Kubernetes manages the rollout by gradually creating and increasing the traffic to new clusters while reducing traffic to old clusters and destroying them.

Kubernetes also provides teams with the ability to detect broken deployment with Readiness probes. These help in ensuring smooth rollbacks for quick recovery from bad deployments. Such rollouts ensure zero-downtime deployments.

Canary deployment requires a deep understanding of the system architecture and hence is best performed in auto-scaling architecture setups.

The auto-scaling feature can automatically add/remove capacity from the resource groups in real-time as per demand. Many cloud providers also allow specifying scaling policies to maintain optimal performance and availability. Scaling policies also help bring better cost control and efficiency in the setups.

Cloud lending platforms provide the kind of support necessary for Canary deployments.

Security and Compliance

Security and Compliance are major areas of interest for Banking systems. Cloud lending platforms can use dedicated Compliance-as-a-Service offerings from leading Cloud providers. This can drastically reduce the cost and efforts required for FinTech firms to abide by local laws and regulations.

In terms of security, Cloud lending platforms often lead the way. AES-256 encryption for data storage and SSL/TLS for data transfers are standards that Cloud providers offer across the board. Apart from this, Leading IAM products like the Cloudflare suite are used to authorise users and control their access policies.

It would cost much more for any on-premise system to match a Cloud lending platform's security and compliance standards.

Cloud lending also lets financial institutions outsource the complex and expensive IT issues of hardware upgrades and software maintenance to the platform providers.

The Best is Yet to Come

With more and more lending institutions adopting Cloud lending platforms like Lentra’s, the speed of innovation has increased many folds. Newer technologies are being experimented with, and GTM strategy timelines are now just a few days in length.

From a technologist’s view, Fintech is where the most exciting changes are happening. At Lentra, we continue to be at the forefront of these technological innovations with our ever-growing product suite.

Schedule a demo with us to know how you can turbocharge your lending workflows.