Transformative Evolution: Credit Integration into the UPI Ecosystem

Discover the future of finance as UPI integrates credit lines. Explore the game-changing 'Credit on UPI,' providing unprecedented financial flexibility for users and a gateway to new opportunities for banks.

In recent years, the landscape of the Indian financial sector has undergone a profound transformation, driven by the rapid embrace of digital technologies. A standout in this evolution is the Unified Payments Interface (UPI), a technological marvel that has reshaped how individuals conduct seamless and instantaneous transactions across diverse platforms.

UPI's impact is already evident in the way people transfer money, settle bills, and make purchases. Adding another layer to this financial revolution, the Reserve Bank, on September 4th, 2023, introduced a circular titled 'Operation of Pre-Sanctioned Credit Lines at Banks through UPI.' This directive enables transactions through a pre-sanctioned credit line issued by a Scheduled Commercial Bank to individuals, with the prior consent of the customer, using the UPI System.

The Integration of Credit into UPI: A Game-Changer

The convergence of credit into the UPI ecosystem is poised to redefine how individuals engage in transactions and manage their finances. Currently, savings accounts, overdraft accounts, prepaid wallets (sometimes intermediated), and credit cards can be linked to UPI. Branded as 'Credit on UPI,' this innovation allows banks to extend credit lines based on their credit policy, specifying terms and conditions for the use of such credit lines, including credit limit, period of credit, rate of interest, etc.

Understanding 'Credit on UPI'

The concept of empowering customers, especially those new to credit, with short-term revolving credit is not entirely novel. The rise of Buy Now Pay Later (BNPL) or Pay-Later solutions in India, such as Paytm Post-paid, MobiKwik Zip, Flipkart ‘Pay-Later,’ and others, leveraged non-banking financial institutions (NBFCs) and banks to extend credit to the underbanked and unbanked segments. 'Credit on UPI' is a feature that allows users of any UPI payment app to access short-term credit on their digital payments. This capability enables users to transition from a semi-closed loop ecosystem (Pay-Later solutions) to a more open-loop one, expanding their financial flexibility.

Benefits for Customers:

- Financial Flexibility: UPI Credit provides customers with a financial safety net, allowing them to make necessary payments even with low account balances, eliminating worries about declined transactions or late fees.

- Convenience: Users can make purchases or pay bills seamlessly, ensuring uninterrupted connectivity, a vital convenience in today's interconnected world.

- Simplified Budgeting: 'Credit on UPI' empowers customers to track credit utilization and manage finances effectively through the UPI app.

- Reward Opportunities: This feature can potentially unlock various reward programs and cashback offers, further incentivizing its usage.

Benefits for Banks:

- Acquiring New Customers: 'Credit on UPI' has the potential to attract new customers to the banking sector, especially those who are not part of the traditional banking clientele.

- Enhancing Customer Engagement: Banks can build stronger relationships with these newly acquired customers by offering tailored credit solutions, ensuring loyalty and sustained engagement.

- Reduced Risk: With shorter tenures and manageable credit limits, UPI Credit minimizes risks associated with lending, presenting an attractive proposition for banks.

- Enhanced Data Insights: Banks can gain valuable insights into customer spending patterns and creditworthiness, enabling them to customize their products and services accordingly.

- Reduced Operational Costs: The digital nature of 'Credit on UPI' streamlines credit processes, potentially reducing operational costs for banks.

How to Activate & Link?

At the time of writing this article, only the BHIM APP allows linking of the ‘Credit limits’ on UPI and going forward likes of GPAY, PAYTM & PAYZAPP will join. As per the BHIM APP, only pre-sanctioned credit limits given by ICICI Bank and HDFC Bank can be linked for now and similar facilities will extended by Axis Bank, PNB AND SBI soon. Here is the step-by-step process to link credit limits given by ICICI Bank over the BHIM APP.

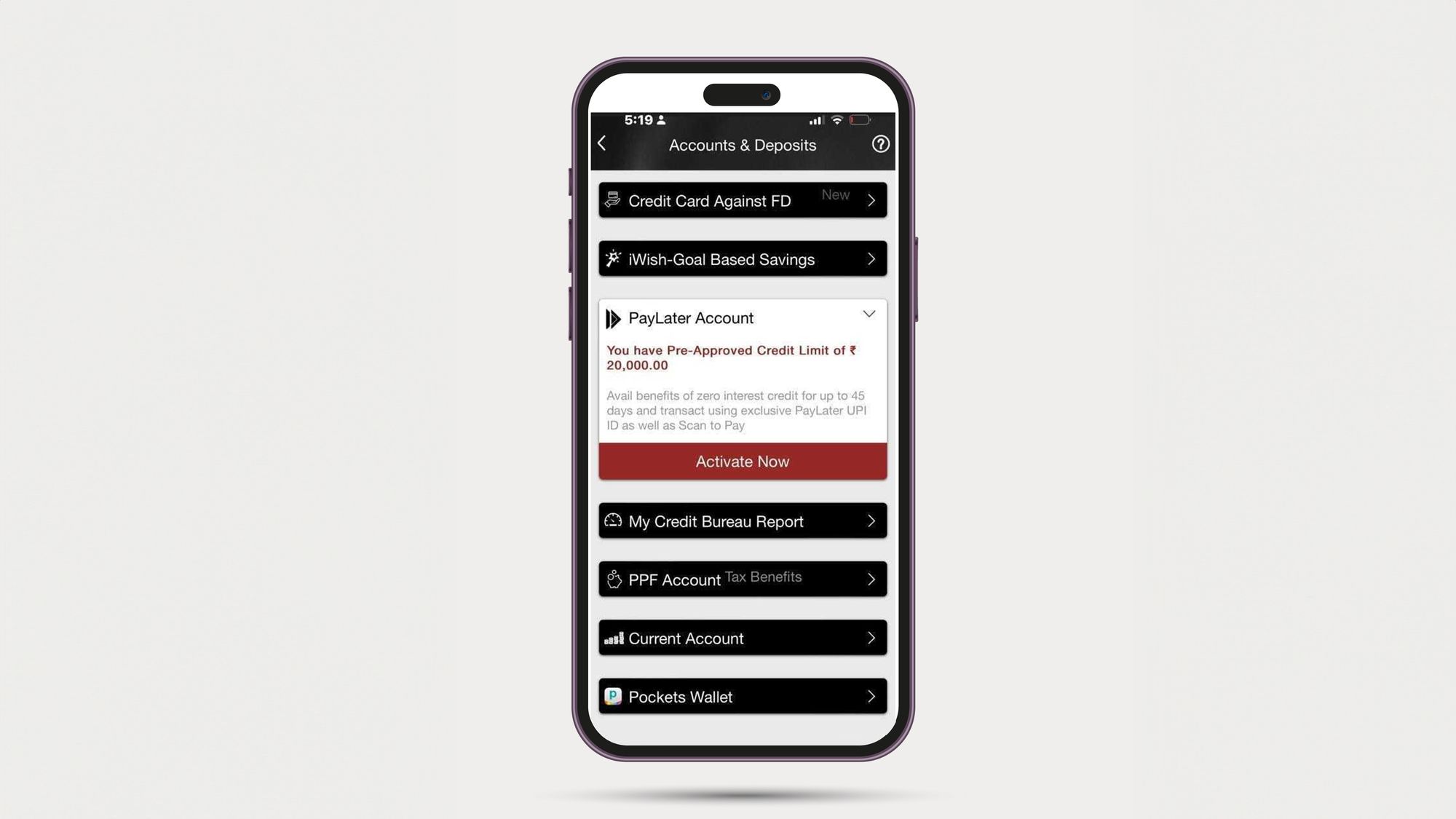

Step 1> Log-in to your ICICI Bank mobile APP and go to the ‘Accounts & Deposits’ section. A new option ‘PayLater Account’ has been added there. Check if some limits have been pre-approved for your account. If yes, then activate the same.

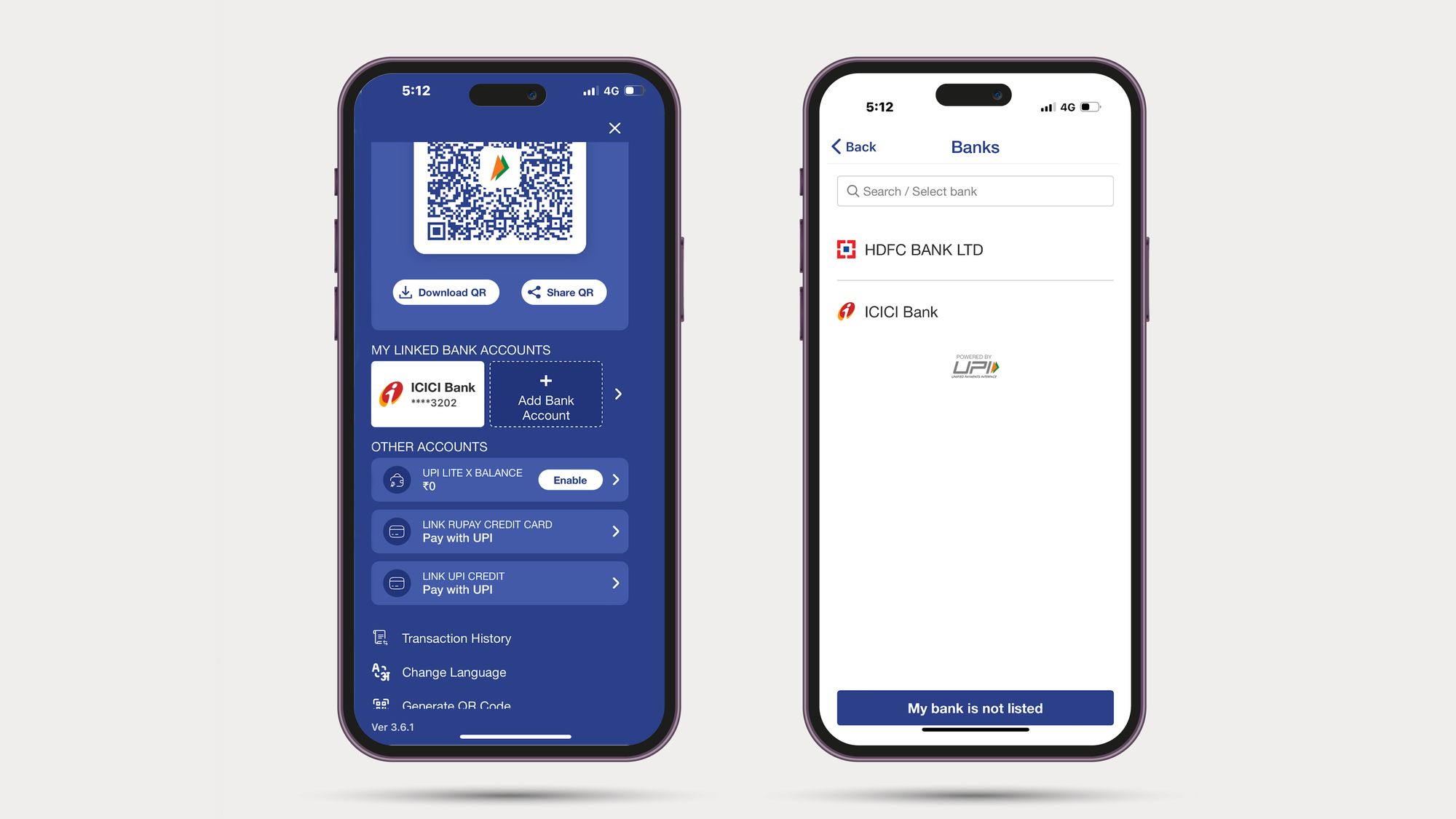

Step 2> Go To BHIM APP and link the limits by accessing ‘Link UPI Credit’ feature from the APP drawer. In the next step, you will be prompted to select your bank. For now, only ICICI Bank and HDFC Bank are available. Once selected, it will automatically search your ‘PayLater’ account and link. Upon linking, you will be able to use the limits.

Conclusion: A Pivotal Step in India's Digital Financial Journey

The integration of credit into the UPI ecosystem marks a significant leap forward in India's digital financial landscape. 'Credit on UPI' empowers customers with unparalleled financial flexibility and convenience while presenting banks with opportunities to expand their reach and deepen customer engagement. As this innovative feature gains traction, it is expected to play a pivotal role in shaping the future of financial transactions in India.

It's worth noting that 'Credit on UPI' poses a significant challenge to existing pay-later offerings, given its innovative edge and potential to capture a substantial market share compared to traditional banking methods. The evolution continues, promising a more inclusive and digitally empowered financial future for all.

How can Lentra Help?

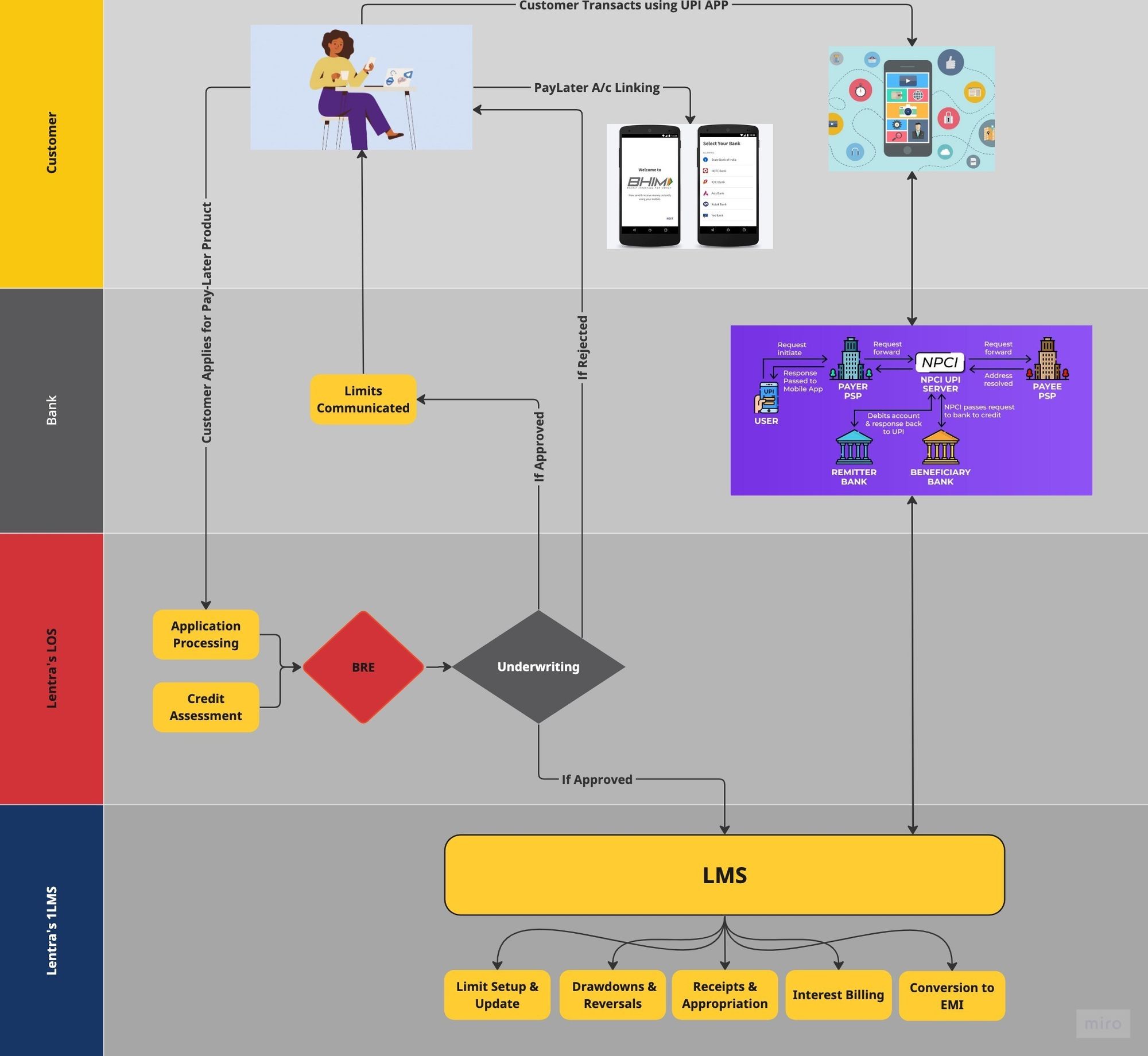

Visual Representation of the entire ‘PayLater’ loan flow from application till loan servicing:-

Lentra 1LMS can seamlessly integrate with the Bank ecosystem(LOS & CBS) for real-time data exchange. The underlying architecture is micro-services based with an option to go multi-cloud or hybrid as per the requirements. 1LMS can easily support up to 700 TPS on a minimal infra setup which makes it highly scalable and resilient. Please refer to the salient features which can help service ‘PayLater’ loans:-

- Onboarding of customers and limits- Revolving and further segregated into Purchase and Cash limits with fungibility(One or both ways) options.

- Tranche drawdowns/reversals- Micro-services-based architecture steered using a robust workflow engine allows authentication and posting of entries on a real-time basis(As soon as the customer does a transaction on the UPI network). 1LMS also supports reversal postings for transactions which for some reason don’t get completed over the UPI network.

- Interest Accruals & Posting- Options to accrue interest daily and post on month-end or any specific due date is another feature of 1LMS. The complex interest calculations algorithm discounts the reversals and calculates the daily reducing balance.

- Pre-closures- Simulation and auto-closure of existing limits is another feature that 1LMS can expose using a set of APIs behind the workflow engine.

- Accepting Payments and Appropriation- 1LMS can accept and appropriate in real-time the payment is done by the customer using the UPI APP over BBPS.

- Showing loan summary-1LMS exposes a set of APIs which can be consumed to show the last 10 transactions, and loan details like overdue, outstanding etc.

- Limits Management and Renewal- Options to renew limits (Auto/Manual) using the API stack and limit management module. LMM or Limit Management is very comprehensive and can help in the conversion of an OD transaction to an EMI loan within the purview of the overall limits and fungibility feature.